Cross-border payments without borders: from SWIFT to emerging rails

9-minute read

Published on: 21 November 2025

Domestic real-time payment networks are in place across nearly 80 markets worldwide. Momentum is building to connect them and, through schemes like OCT Inst and common standards such as ISO 20022, cross-border payments will become just as fast, affordable, and reliable as domestic ones.

The driving force behind this change is customer expectations. From peer-to-peer transfers to mobile wallets, consumers and businesses alike are growing used to real-time payments. They now expect that same instant experience everywhere, whether moving money locally or across borders.

Yet many traditional banks remain constrained by legacy systems not built for today’s market demands. And if their payment channels can’t match the speed, resiliency, and transparency clients are accustomed to, their cross-border offering quickly becomes a liability. Beyond the payments engine itself, supporting functions like liquidity management, compliance, and customer service must also evolve to operate in real time.

The stakes are high. Valued at $212.5 billion in 2024, the cross-border payments market is expected to reach $320.7 billion by 2030, growing at a CAGR of 7.1%. If they want to capture their share of that growth, banks will need to modernize their cross-border capabilities. In this article, we’ll explore:

- The biggest challenges in cross-border payments

- Emerging rails worth looking at

- How Payment Central helps banks tackle cross-border challenges

The biggest challenges in cross-border payments

As the industry pushes towards real-time, cross-border transactions, banks face a growing set of challenges, from choosing the right rails to keeping pace with fintech competitors.

Difficulty optimizing for the best payment rails to balance compliance, cost, and speed

One of the biggest challenges banks face is optimizing payment rails to process cross-border payments efficiently. Every payment has three critical dimensions that must be considered:

- Compliance: Different countries and payment rails have varying regulatory requirements. Banks need to ensure every cross-border transaction, whether low-value or high-value, meets the relevant standards. For example, if their domestic market mandates participation in a new payment rail, such as Fedwire in the U.S. or TARGET2 in Europe, the bank must prioritize this.

- Cost: Banks also have to consider the cost of each payment rail. For instance, while the true cost of a SWIFT message is pennies, the additional banking charges that cover network, application, and resource costs can make a SWIFT transfer expensive. Choosing the wrong rail can quickly eat into margins.

- Speed: Settlement times can vary depending on the payment rail. A SWIFT transfer can take anywhere from a few days to a week, while other rails like EPA Instant in Europe or Faster Payments in the UK can be near-instant. In addition to compliance and cost, banks also need to consider which rail can deliver the efficient, timely experience clients expect.

- Effectively balancing these three factors must happen in real time. For banks, this means modernizing systems to automatically route each transaction along the most efficient, cost-effective, and compliant path.

More payment rails mean greater complexity in payment reconciliation

Modern rails are critical for keeping up with market demands, but they also introduce operational burdens. The more payment rails a bank manages, the more complex it becomes to track and reconcile payments.

Each transfer – whether it’s a letter of credit, peer-to-peer payment, or bank-to-bank transaction – must be properly linked, verified, and reconciled with internal systems. As the number of rails increases, so does the risk of delays, failed payments, or misapplied funds.

As banks expand their payment options, they must carefully consider how their reconciliation and tracking processes will scale to handle multiple currencies, jurisdictions, and regulatory requirements.

Reliance on legacy systems limits agility

Legacy systems, often built decades ago, weren’t built to handle the speed, complexity, and variety of today’s cross-border payments.

Part of the challenge in updating these systems is cultural. Some traditional banks still prefer to build solutions in-house rather than partner with fintechs or adopt newer, specialized platforms. While this approach can feel controlled, it comes at a cost.

It’s expensive, complex, and time-consuming to outfit legacy systems for modern payment rails. In fact, 60% of payments IT budgets are spent on maintaining compliance, budget that could otherwise fund innovation, improve operational efficiency, or upgrade the client experience.

Rising competition from fintechs that move faster and market better

Fintechs and challenger banks continue to raise the bar for speed, customer experience, and product innovation. Their ability to launch services quickly, experiment at scale, and market with precision has reshaped consumer expectations. Traditional banks risk fading into the background – becoming the regulated infrastructure layer – while fintechs own the customer relationship, brand visibility, and engagement.

To illustrate the pace and scale of change:

| Company | Customers | Assets / Deposits | Growth Speed | What Drives Advantage |

| Revolut | 60M+ globally | ~$38 B balances | ~38% user growth YoY / ~72% revenue growth YoY | Data-driven product launches, global scale, viral growth engine |

| Trade Republic | 8 M | €100 B+ AUM | Scaled to 8 M users in ~6 years | Mobile-first investing, rapid feature delivery, low-cost model |

| Tier-1 European Bank (typical) | 5M–25M | €300 B–€2 T+ | Gradual digital adoption, multi-year transformation cycles | Trust and scale, but slower execution and legacy stack constraints |

These numbers highlight a clear dynamic: success is less about balance sheet size and more about speed, engagement, and data activation.

Revolut now serves over 60 million customers across 50 markets – exceeding the reach of many major European banks – despite a smaller deposit base and revenue. Its advantage lies in continual data utilisation, rapid product release cycles, and a strong digital brand that drives daily engagement and loyalty.

For banks to remain visible and relevant, they need platforms and operating models that enable faster innovation, embedded intelligence, and rapid go-to-market, so they can match fintech pace without compromising trust or stability.

How emerging rails can unlock faster cross-border payments

A key part of delivering real-time payments to demanding customers is testing and adopting emerging payment rails. These rails give banks a chance to tap into systems that are faster, more cost-effective, and better aligned with changing expectations.

Over the years, as demand for real-time, cross-border payments surged, established rails have evolved to stay competitive. SWIFT, for instance, introduced new product features like Swift GPI and Swift Go to provide customers with new payment and reconciliation capabilities.

At the same time, new rails have emerged that bring greater cost efficiency and speed to cross-border transactions:

- Blockchain-based payment rails and digital currencies like stablecoins promise more affordable, faster, and more secure transactions.

- Card networks such as Visa and Mastercard have expanded into B2B and cross-border payments.

- Regional real-time payment systems – like Pix in Brazil and UPI in India – are exploring collaborations to link markets and create faster global ecosystems.

These emerging rails can make cross-border payments cheaper and less complex for banks – but implementing them requires a modernized payment infrastructure.

How Payment Central helps banks tackle cross-border challenges

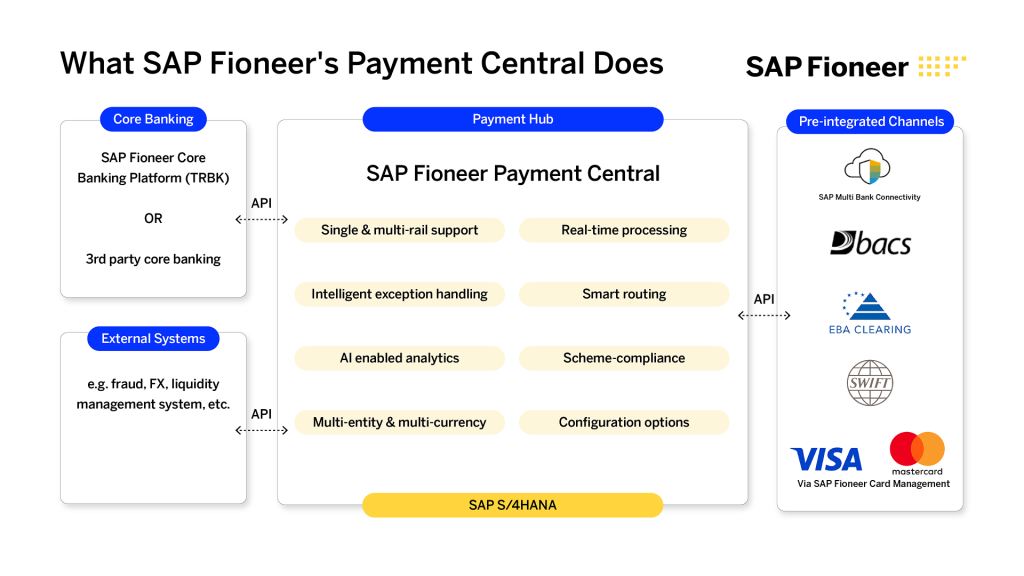

SAP Fioneer’s Payment Central is a standalone hub built to handle diverse real-time, cross-border payment flows across multiple channels 24/7. It’s core-agnostic, meaning it integrates with any core banking system – whether SAP Fioneer’s own or third-party – using flexible APIs and templates for fast onboarding and low disruption.

Here’s how Payment Central helps banks simplify operations, gain end-to-end transparency, and power innovation.

Easily add new payment instruments and optimize payment path selection

As mentioned previously, a key aspect of solving cross-border payments is correctly balancing compliance, cost, and speed when choosing which payment rails to implement and use for each payment.

Payment Central helps strike that balance through automated path selection and built-in compliance standards that ensure each payment is routed optimally according to business rules, cost priorities, or speed needs.

Payment Central also provides pre-integrated support for major schemes like SWIFT, BACS, Visa, and Mastercard, as well as for ISO 20022 and legacy SWIFT MT formats. With a single platform, banks can gain multi-rail flexibility, making it easy to add emerging rails such as stablecoins or regional real-time payment networks.

Payment Central’s modular design makes it a versatile solution for banks of any size. It’s not all or nothing – banks can tailor and configure it to meet their exact needs.

For example, a tier-one bank can use Payment Central to handle many cross-border payments daily with full transparency and speed, while a smaller bank might use it to connect a single SEPA or SWIFT rail without disrupting existing systems.

Access a unified platform that connects departments and entities for greater transparency

Managing multiple payment rails can quickly create operational complexity and make reconciliation slow, error-prone, or costly.

Payment Central addresses this by being a unified hub that connects treasury, cash management, and other payment-related departments through API integrations. A centralized dashboard provides a complete view of all payment flows, exceptions, alerts, and SLAs, giving teams the end-to-end transparency they need to act quickly and confidently.

With multi-currency and multi-entity support, Payment Central is ideal for global banks:

- Process and reconcile payments in any currency with built-in conversion logic and cross-entity transparency.

- Support different brands, subsidies, or legal entities with configurable access, processing rules, and reporting.

- Ensure immediate compatibility across countries, formats and schemes with customizable templates.

By centralizing visibility and control, banks can scale cross-border payments without increasing operational complexity.

Use low-code/no-code product configuration to accelerate implementation

When only developers can make system changes, it slows implementation down for everyone. Legacy infrastructures further compound the issue, limiting banks’ ability to quickly process complex cross-border payments and get ahead of changing market demands.

Built natively for SAP S/4HANA, Payment Central enables high-speed, high-volume processing with real-time visibility. This ensures unmatched performance for domestic, cross-border, and even CBDC-ready payments.

Payment Central also makes it easier for teams to launch and adapt payment services with low-code tools and configurable business logic. New products, rails, and formats can be launched up to 4x faster, letting banks respond to customer expectations and competitive pressure without overhauling legacy systems.

Banks must modernize infrastructure to deliver faster, more efficient cross-border payments

Success in real-time payments requires cross-border capabilities that are equally as fast, reliable, and efficient.

SAP Fioneer’s Payment Central is a centralized payments hub that makes cross-border processing simpler and smarter. Built-in compliance, pre-integrated schemes, and optimized path selection reduce the complexity of adding new rails, while low-code / no-code tools let teams roll out new services fast.

Request a demo today to see how Payment Central can help your bank deliver faster, more efficient cross-border payments and future-proof its operations.

Related posts

Wie KI die Effizienz im Zahlungsverkehr neu definiert

ISO 20022 – The decade-old standard banks still aren’t ready for

Real-time payments – always on, but are banks always ready?

Most read posts

What sets modern policy administration systems apart

Unlocking scalable AI in insurance from the core

Virtual account management: the quick win for a stronger cash management proposition

More posts

Get up to speed with the latest insights and find the information you need to help you succeed.